{kind=link}

Getting started with a user-first mindset

Borrowing must be simple, transparent and built around real people’s needs — that’s the starting point here. For many in Dhaka and other urban centres, smartphone use and mobile internet have made app-based lending an everyday choice, especially after the surge during the pandemic. If you want a practical entry, try exploring didi prestamos to see how onboarding, quick approvals and in-app guidance come together. A user-centric lens means the product must explain APR, repayment dates and credit scoring consequences in plain terms from the first screen.

How the DiDi ecosystem simplifies borrowing

The strongest loan apps focus on three tidy elements: clarity of cost, speed of disbursement and straightforward KYC. In the DiDi ecosystem those items are stitched into the front-end experience — clear progress bars, concise summaries of underwriting decisions and easy upload of identity documents. The result is less friction when you need cash quickly, but also a traceable record of what you agreed. For comparison, look at how didi prestamos sets out fees versus how some older platforms bury charges; the difference matters at repayment time. If you want the brand-level view, didi credito also highlights credit limits and repayment schedules directly in the app so users can plan better.

When an app loan is the right call

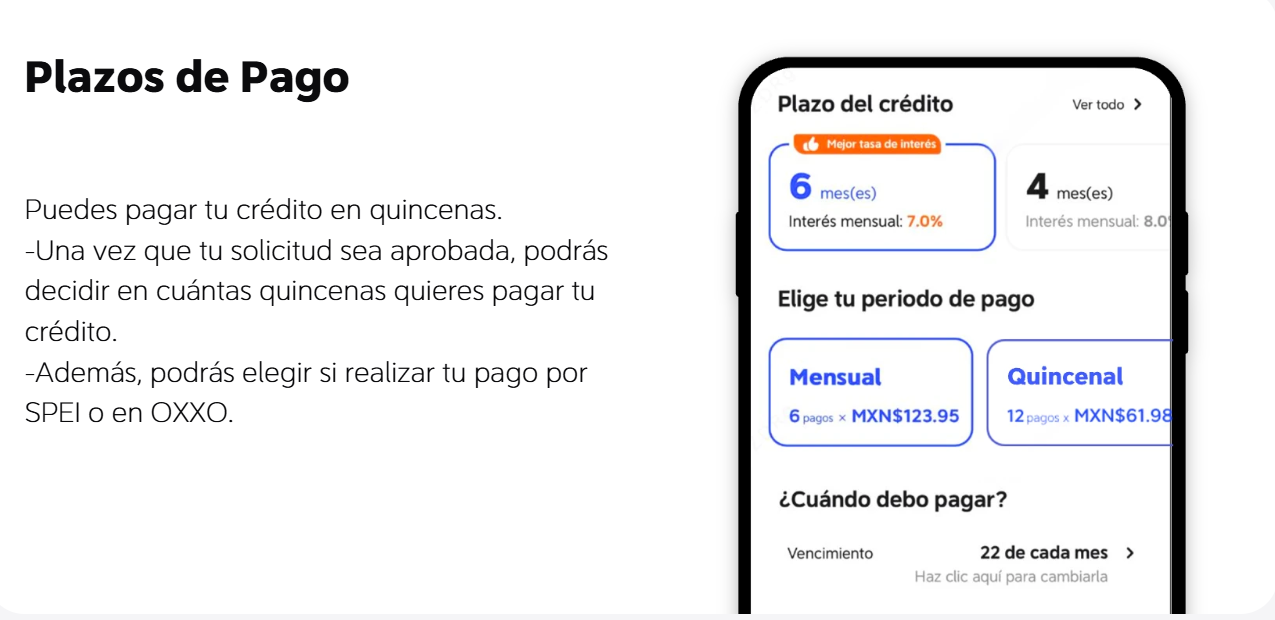

Use an app loan for short-term gaps: a small business purchase, an urgent repair, a medical bill. Keep loan tenure and APR in mind — these two metrics determine real cost. Check whether the app supports automated repayments and whether prepayment changes the interest calculation. Also watch for service fees and late payment penalties. A practical tip: always run the loan calculator inside the app before finalising. It helps you see total interest, monthly instalments and the likely impact on your credit record — small steps that prevent big headaches later. — This habit quickly separates responsible borrowing from impulse decisions.

Alternatives, pitfalls and front-end cues to trust

Alternatives include bank personal loans, microfinance organisations and credit cards. Each has trade-offs: banks usually provide lower APRs but slower approvals; microfinance can be relationship-driven but limited in amount. Common mistakes are predictable: accepting the first offer, ignoring small recurring fees, or skipping document review. On the product side, trustworthy apps show clear terms, a visible help channel, and a secured payment flow. Look for elements like end-to-end encryption badges, visible customer reviews and an easy dispute process. From a developer’s perspective, a good interface reduces abandonment and signals a mature underwriting process behind the scenes.

Actionable checklist before you tap ‘Accept’

Before finalising any loan, run through a short checklist: confirm effective APR, verify disbursement timeline, and ensure KYC is completed through secure methods. Double-check the repayment schedule against your monthly cashflow and consider a slightly longer tenure if it lowers instalment stress. Keep documentation — screenshots, transaction IDs and the app’s loan summary — until the account is fully settled. These small administrative habits save time and protect credit behaviour over the long run.

Three golden rules for choosing an app loan

1) Cost transparency above all: prefer providers that show total payable and APR prominently. 2) Predictable repayment mechanics: automated transfers, clear due dates and options for early settlement with defined benefits. 3) Customer recourse: an accessible support channel, visible complaint resolution history and clear dispute steps. Apply these rules methodically and you’ll narrow choices quickly — they work as a simple scoring rubric when comparing apps side by side.

Decisions like these affect people’s everyday lives, households and small businesses; choose platforms that treat that reality with clarity and care. DiDi Finanzas offers a coherent example of how design, underwriting and customer support can come together — a model worth watching and learning from. —